- Banks Must Innovate to Keep Young Customers from Embracing Web Rivals

- For Banks, an Alibaba Warning

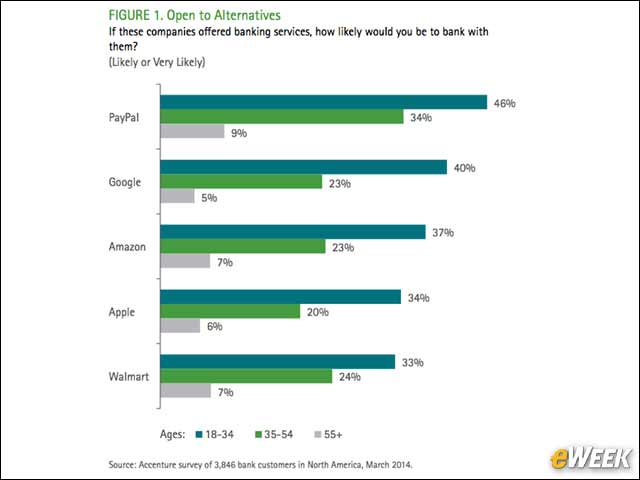

- Customers Are Open to New Ideas

- The Mobile Payments Space

- False Comforts and Challenges

- Bad Time for Bad News

- But There’s Good News

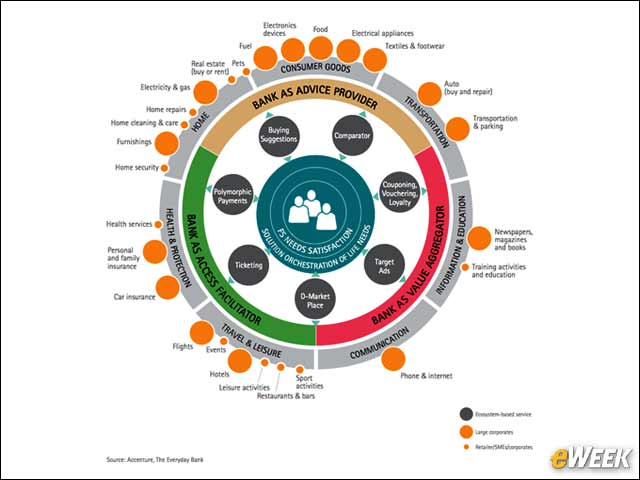

- Using Advantages to Benefit

- Take a Lesson from Apple, Alibaba and Google

- Consumers Want Analysis and Advice

- Leading by Example

Banks Must Innovate to Keep Young Customers from Embracing Web Rivals

by Michelle Maisto

For Banks, an Alibaba Warning

Amazon “made waves” in 2012 when it began offering merchant loans, but it was already three years behind China’s Alibaba. By offering savings account interest rates up to 15 times higher than standard banks, within nine months it had the equivalent of 20 percent of all new deposits in China, according to the Accenture report.

Customers Are Open to New Ideas

Companies are increasingly looking for profits in new industries; Apple, for example, became the world’s largest music retailer in just seven years, Accenture points out. When asked how likely they were to bank with popular mobile brands, should services be offered, consumers—especially Millennials, but even those in their 40s and 50s—proved to be very open.

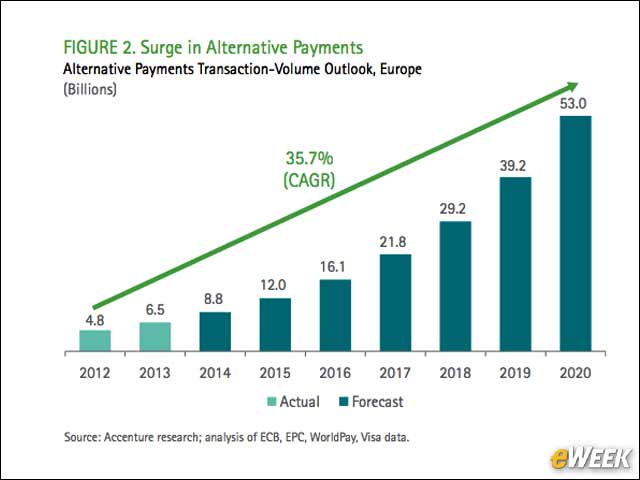

The Mobile Payments Space

Banks have traditionally generated up to 25 percent of their revenues from mobile payments; today, PayPal leads that space. Google offers a plastic debit card to go with its mobile wallet, T-Mobile now also offers banking services and Square has gained 4 million-plus users since 2009. Banks told Accenture that the biggest structural challenges of the next five years are increased regulation, technology and the ability to reshape industry boundaries.

False Comforts and Challenges

Regulation used to be a barrier to entry in the banking business, according to Accenture, but not anymore. “Some new entrants have grown rapidly without ever becoming regulated banks at all,” the report said. “Google Wallet, T-Mobile, PayPal, Simple and Moven have all relied on the ‘white-label’ services of The Bancorp to provide regulated services to their customers.”

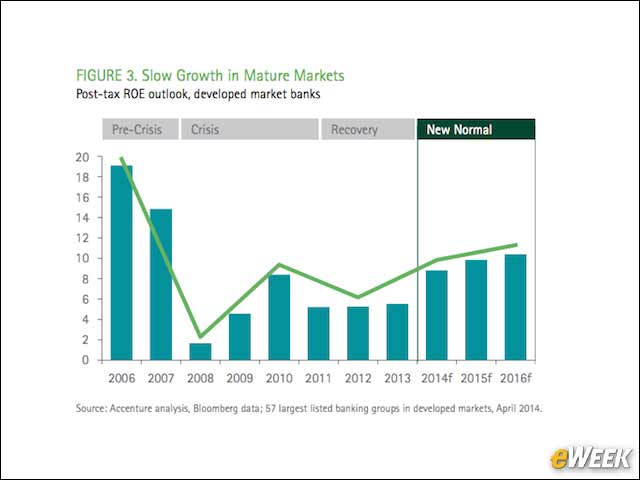

Bad Time for Bad News

Slow growth and high regulatory costs are expected to hold down return-on-equity, Accenture said. While growth is strong in emerging markets, customers in those markets are less loyal. Banks also face the need to update old back-office systems, which are increasing the costs of modern customer-facing solutions. While alternative payments may be enticing to a bank’s digital units, its card division “may see it as little more than a way to cannibalize revenues,” the report said.

But There’s Good News

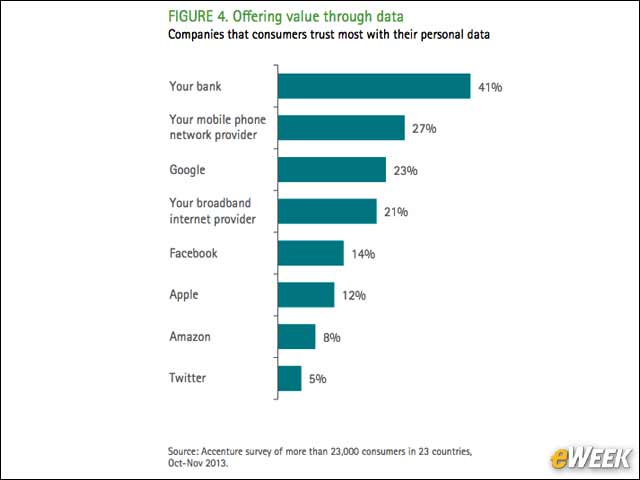

Banks are in the advantageous position of having valuable know-how in the field of payments, security and compliance, as well as information about customers and the transactions they make. And while the public doesn’t rate banks well, it does trust them. It’s the industry that customers trust most in their lives.

Using Advantages to Benefit

“New analytic technologies make it possible for banks to use transaction data to deliver savings to customers and bring revenue—all from safe within their four walls,” the report said. But first, banks must focus on “earning the right to a deeper commercial relationship” by being transparent and offering “opt-in” benefits.

Take a Lesson from Apple, Alibaba and Google

Banks need to enhance conveniences and the quality of everyday life for customers—just as Apple, Amazon, Alibaba and Google aim to, Accenture said. “They must learn to play a greater role, not just at the moment of financial transaction but before and afterwards, as well.” For example, they could combine their transactional data with tools that help customers make buying decisions, whether for a new car or dinner.

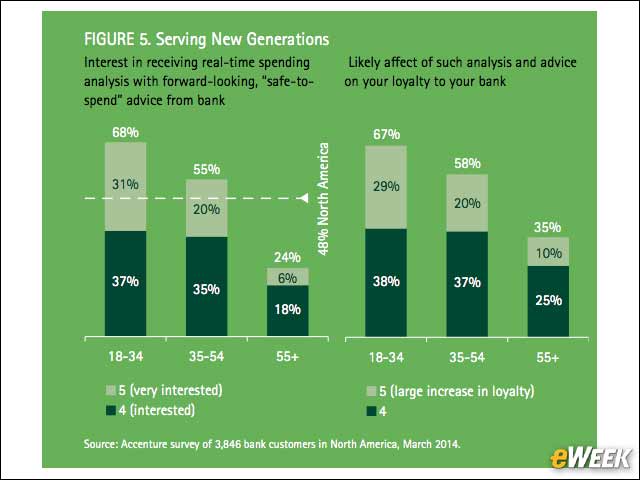

Consumers Want Analysis and Advice

In North America alone, 68 percent of consumers ages 18 to 34 say they would “welcome receiving things like a ‘safe-to-spend’ analysis from their bank.” Almost as many people said it would make them more loyal to their banks.

Leading by Example

Accenture highlighted Garanti, Turkey’s second-largest bank, as an example of an “Everyday Bank” leader. Its iGaranti app offers savings suggestions, analyzes spending patterns to provide customized merchant discounts, and lets users withdraw cash using a QR code on their phone, instead of an ATM card. In short, it offers day-to-day value by going beyond “mere banking and payments,” Accenture said.