Digital technologies are erasing the boundaries between industries while companies searching for new revenue streams are looking in new markets. If you add to this consumers’ deepening relationships with leading mobile companies, and traditional banks are in trouble, according to a new report from Accenture.

The company surveyed more than 4,000 retail bank customers in the United States and Canada and found significant numbers of them open to switching to branchless banks, as well as to banking with trusted mobile brands.

Were Google to offer banking services, 40 percent of 18- to 34-year-olds said they would be likely or very likely to bank with it. In the case of Apple, 34 percent of the peer group said the same, while 37 percent said the same about Amazon and 46 percent were on board with PayPal.

The idea was also far from unheard of among 35- to 54-year-olds, who felt most confident banking with PayPal (34 percent), though even the company that placed fifth, Apple, had the backing of 20 percent of the peer group.

“Tomorrow’s consumer is coming of age with a very different perception of what a bank could be,” Wayne Busch, managing director of Accenture’s North American Banking practice, said in a May 27 statement. “Those expectations could become profoundly disruptive to banks if non-bank entrants gain momentum and banks fail to adapt quickly.”

Accenture advises that banks engage what it calls the “Everyday Bank strategy.” Much of this entails banks stretching beyond financial transactions and positioning themselves as “trusted partners” within consumers’ lives and within an ecosystem of services that benefit consumers on a day-to-day level.

More than half of the 18- to 34-year-olds surveyed (55 percent) said they’d like banks to help with the “heavy lifting” of big purchases, like cars.

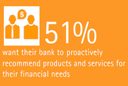

Even more people wanted services to help them make much smaller spending decisions; 68 percent of the same peer group said they’d be interested in real-time analysis of their spending, including “safe-to-spend” forecasts, while 55 percent of 35- to 55-year-olds said the same. Further, 67 percent and 58 percent of the respective peer groups said such a service would make them more loyal.

“Banks have a unique understanding of the transactions carried out between customers and merchants. Going forward, this transactional information will be one of their greatest assets—allowing them to understand their customers better, provide them with value-added services, and facilitate commerce in new ways,” states the report.

Despite the reputational damage banks suffered during the financial crisis, the report adds, consumers still trust banks with their personal data more than they trust any other companies.

Accenture’s Everyday Bank strategy insists banks need to collaborate with other organizations to put themselves at the center of an extended ecosystem.

Everyday Banks also need to be access facilitators, helping customers to discover products and services that are relevant to them; value aggregators, offering merchant-backed rewards through loyalty programs and programs based on volume and scale; and advice providers, using the insights they have to help customers better manage their money and deal with financial milestones.

While banking was once about transitions, people are now seeking advice and relationships, said Robert Mulhall, a managing director in Accenture Distribution and Marketing Services.

“In this digital era, the most successful companies focus on solutions, rather than products, to simplify their customers’ everyday lives,” added Mulhall. “Banks also need to think this way.”