IT industry authority Synergy Research Group reported Jan. 4 that across six key enterprise infrastructure hardware segments, vendor revenues for the last four quarters increased by nearly 3 percent.

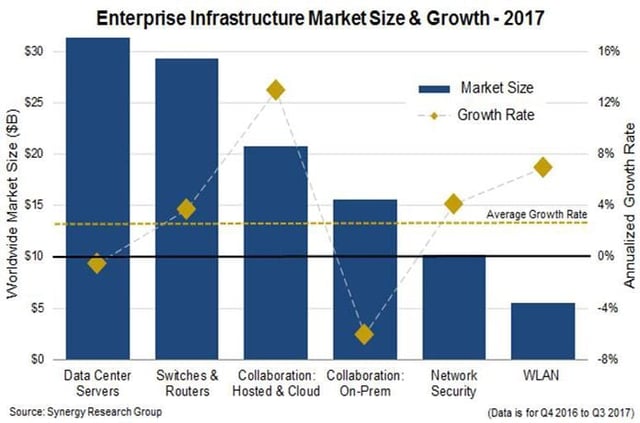

Aggregate revenues for the calendar year 2017 reached $113 billion, with revenue in each of the last 12 quarters typically in the $26 billion to $29 billion range. Data center servers comprise the largest segment of the market, although revenues in that market declined by about 1 percent in 2017.

Switches and routers, the second-largest segment, reported 4 percent growth. In that category, hosted and cloud collaboration networking equipment grew the most, while on-premise collaboration continued to be challenged by aggressive price competition and market disruption.

(Editor’s note: If you’re using a laptop or desktop computer, you can expand the size of the chart at left by right-clicking on the image and selecting “View Image.”)

Cisco Systems, the world’s largest internet networking equipment manufacturer with a market cap value of $194 billion, remains the dominant enterprise vendor. The San Jose, Calif.-based company is the market leader in four of the six segments, with the exceptions being hosted and cloud collaboration, where it is ranked second, and data center servers, where it is fifth.

Cisco Systems Owns 26 Percent of Entire Market

In aggregate across the six segments, Cisco’s market share during the last four quarters was 26 percent, which was down a percentage point from the preceding four quarters.

Hewlett-Packard Enterprise, the No. 2-ranked enterprise vendor, came in with a market share of 11 percent across the six segments. It is No. 1 in sales of data center servers, No. 2 in WLAN equipment and third in switches and routers, Synergy reported.

Hosted and cloud collaboration hardware is the one area where neither Cisco nor HPE are the top vendor; Microsoft is the leader in this segment. The No. 2-ranked vendors in the other segments are Dell EMC (enterprise data center servers), Huawei (switches and routers), Microsoft (on-premise collaboration) and Check Point (network security).

Major vendors that have achieved high 2017 growth rates in these highly competitive markets include Super Micro, Arista Networks and RingCentral, Synergy said.

Infrastructure Spending ‘Will Stay on the Rise for Five Years’

“Despite a burgeoning public cloud market, enterprise IT infrastructure spending was still on the rise in 2017 and will be for the next five years,” Synergy Research Group founder and Chief Analyst Jeremy Duke said. “The focus of that spending is changing, however, with a growing emphasis on hosted solutions, subscription-based business models and emerging technologies.

“Those changes will continue to present challenges for incumbent vendors and opportunities for new market entrants.”

Synergy provides quarterly market sizing and segmentation data on a range of enterprise infrastructure markets, including vendor revenues by segment and by region.