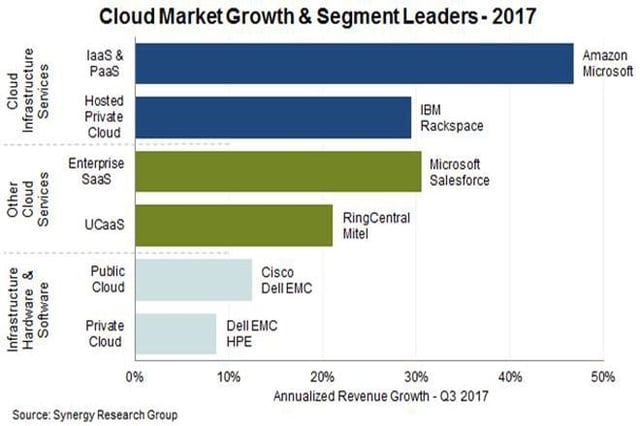

New IT market data released Jan. 4 by Synergy Research Group shows that across six key cloud services and infrastructure market segments, operator and vendor revenues for the four quarters ending September 2017 reached $180 billion, having grown by 24 percent on an annualized basis.

IaaS (infrastructure as a service) and PaaS (platform as a service) had the highest growth rate at 47 percent, followed by enterprise SaaS (software as a service) at 31 percent and hosted private cloud infrastructure services at 30 percent.

2016 was notable as the year in which enterprise spending on cloud services overtook that of hardware and software used to build public and private clouds, Synergy said. In 2017, the gap widened. In aggregate, cloud service markets are now growing more than three times faster than cloud infrastructure hardware and software.

Companies among the most prominent in the 2017 market segment were the usual suspects: Amazon/AWS, Microsoft, IBM, Salesforce, Dell EMC, Hewlett-Packard Enterprise and Cisco Systems.

(Editor’s note: If you’re using a laptop or desktop computer, you can expand the size of the chart at left by right-clicking on the image and selecting “View Image.”)

During the period Q4 2016 to Q3 2017, total spending on hardware and software to build cloud infrastructure approached $80 billion, split evenly between public and private clouds–though spending on public cloud is growing more rapidly.

Infrastructure investments by cloud service providers helped them to generate more than $100 billion in revenues from cloud infrastructure services (IaaS, PaaS, hosted private cloud services) and enterprise SaaS – in addition to which that cloud provider infrastructure supports internet services such as search, social networking, email, e-commerce and gaming.

Meanwhile, unified communications as a service (UCaaS)–in many ways a different type of market–is also growing strongly and is driving some radical changes in business communications.

“We tagged 2015 as the year when cloud became mainstream and 2016 as the year when cloud started to dominate many IT market segments. In 2017 cloud was the new normal,” Synergy Chief Analyst and Research Director John Dinsdale said.

“Major barriers to cloud adoption are now almost a thing of the past, with previously perceived weaknesses such as security now often seen as strengths. Cloud technologies are now generating massive revenues for cloud service providers and technology vendors and we forecast that current market growth rates will decline only slowly over the next five years.”

Synergy provides quarterly market sizing and segmentation data on cloud and related markets, including company revenues by segment and by region.